Image By: Shaili Shah

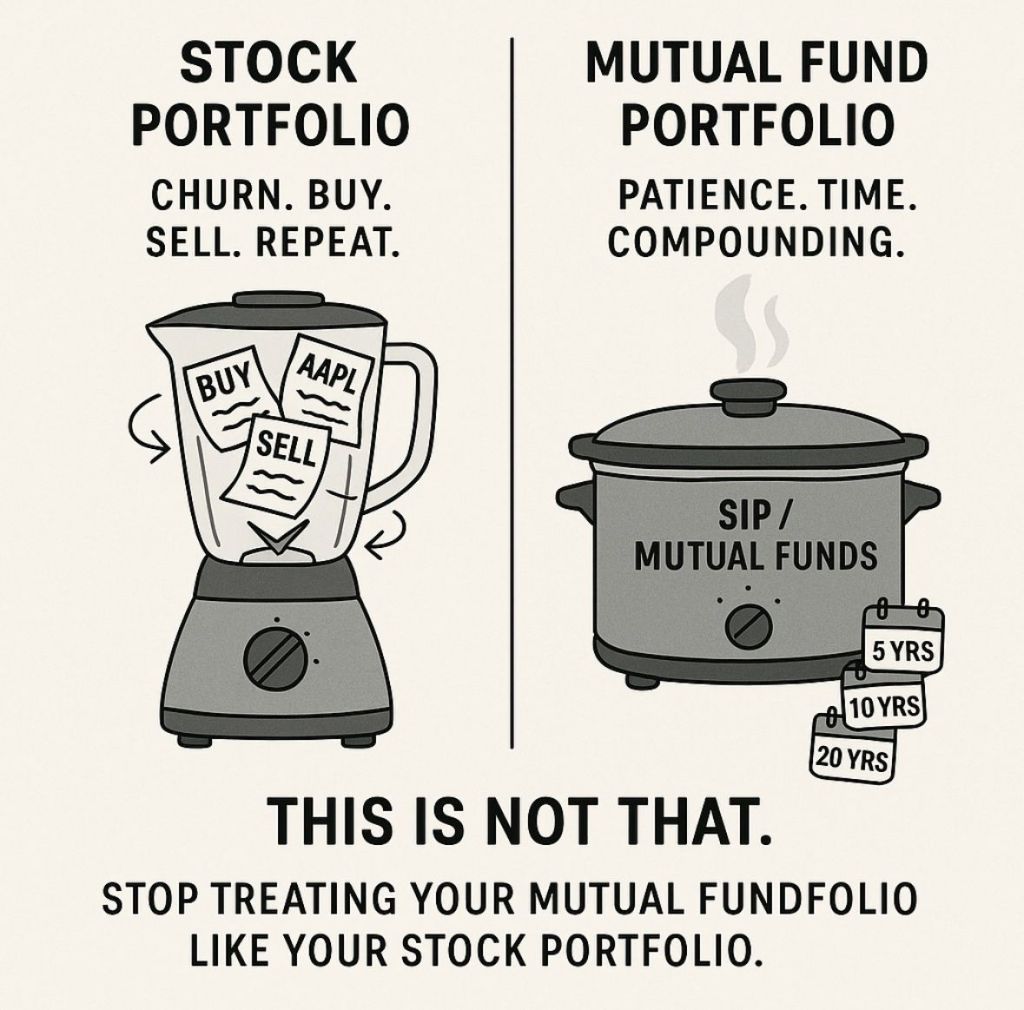

I had a conversation with someone, and one pattern I’ve noticed repeatedly is how people treat their mutual fund investments like stock trading accounts—chasing quick profits, reacting to every market swing, or jumping into trending funds based on recent performance. This approach often leads to costly mistakes that can derail financial goals. Drawing inspiration from the timeless wisdom shared on Value Research Online’s First Page, where Dhirendra Sir emphasizes disciplined, long-term investing, I’ll explain why mutual funds and stock trading are fundamentally different, how confusing them hurts your wealth-building journey, and why patience is your greatest asset.

The Hype Cycle: A Common Mistake

I’ve seen friends, readers, and even seasoned investors get caught in what I call the “hype cycle.” A mutual fund posts stellar returns, or a stock skyrockets, and suddenly everyone thinks, “I need to invest now!” For instance, when a fund gains 20% in a few months, people rush to pour money in, fearing they’ll miss out. Conversely, when markets dip, like during the October 2024 market wobble discussed on First Page, many panic and sell their holdings to “cut losses.” This is recency bias—our tendency to overemphasize recent events and lose sight of the long-term picture. It’s like avoiding a favorite restaurant because of one bad meal, despite enjoying it for years.

This behavior is amplified by today’s constant stream of market updates on apps, X posts, or financial influencers pushing the latest “hot” investment. For younger investors, the urge to act on every market move can feel intense. But as Dhirendra Sir often stresses in his First Page columns, chasing short-term trends or reacting to market noise is a surefire way to undermine your financial goals. Mutual funds and stock trading serve different purposes, and treating them the same is a costly error. Let’s explore why.

Stock Trading: The High-Risk Sprint

Stock trading is like a high-speed sprint—fast, thrilling, and risky. When you buy individual stocks, you’re betting on specific companies, aiming to time the market by buying low and selling high. It’s exciting when a stock like Reliance Industries jumps 15% in a month, but it’s nerve-wracking when it drops 10% due to a market rumor or global event. Success requires deep research, constant monitoring, and a knack for predicting market moves—a skill even professionals struggle with. As Dhirendra Kumar noted in a First Page article, “Market soothsayers have two lists of reasons: one when the market goes up, another when it goes down,” highlighting how unpredictable stock trading can be.

For example, imagine you invest ₹1,00,000 in a single stock like Zomato. If it surges 25% in a month, your investment grows to ₹1,25,000—thrilling! But if it crashes 20% the next month due to a bad earnings report, you’re down to ₹80,000, and the stress kicks in. This volatility demands time, expertise, and emotional resilience, which most investors—especially those new to the game—don’t have.

Mutual Funds: The Steady Marathon

Mutual funds, by contrast, are like a marathon—steady, deliberate, and built for endurance. They pool your money with others’ and invest across a diverse range of assets, like stocks, bonds, or both, managed by professionals. This diversification reduces risk, as a bad day for one company doesn’t tank your entire portfolio. As Dhirendra Sir emphasizes in his First Page columns, mutual funds are designed for compounding and long-term growth, not quick wins.

For instance, consider a diversified equity mutual fund like an index fund tracking the Nifty 50. Your ₹1,00,000 investment is spread across 50 major companies, so a 10% drop in one stock, like HDFC Bank, is cushioned by others. If the fund averages 10% annual returns, your ₹1,00,000 could grow to about ₹2,59,374 in 10 years, assuming compounding. The key? You need to stay invested and resist the urge to jump ship when markets wobble, as Dhirendra Sir advises in his Investors’ Hangout webinars.

Why Mixing the Two Hurts Your Wealth

Treating mutual funds like stocks is like using a marathon runner’s strategy in a sprint—it doesn’t work. Dhirendra Sir often warns against this in his First Page writings, noting that “discipline and planning are the most important, not being swayed by WhatsApp/YouTube University.” Here are three ways this mistake can derail your financial goals, with Indian Rupee examples:

- Disrupting Compounding

Compounding is the magic that makes mutual funds powerful, but it needs time. If you invest ₹5,000 monthly in an equity mutual fund via a Systematic Investment Plan (SIP) with an average return of 12%, you could have about ₹23,23,391 after 15 years. But if you keep switching funds or redeeming early because a fund’s short-term returns look “flat,” you halt compounding. For example, pulling out after two years because the market dipped (like in October 2024) might leave you with just ₹1,50,000 instead of letting it grow to millions. Dhirendra Sir stresses sticking to quality funds for the long term to avoid this trap. - Missing Market Recoveries

Markets are volatile—Dhirendra Kumar noted in a First Page piece that October 2024 saw narratives about FIIs shifting to China, spooking investors. If you sell your mutual fund during such dips, you miss the recovery. For instance, if you invested ₹2,00,000 in a balanced fund in early 2020 before the COVID crash, it might have dropped to ₹1,60,000 by March. Selling then would lock in your loss, but holding on could see it recover to ₹3,00,000 by 2022, as markets rebounded. Dhirendra Sir advises ignoring short-term noise and staying invested for long-term gains. - Emotional and Financial Stress

Constantly checking your mutual fund’s daily NAV (Net Asset Value) or chasing trending funds is exhausting. It’s like refreshing your phone for stock price updates—stressful and unproductive. If you invest ₹3,00,000 in a fund and see it dip to ₹2,80,000 in a month, you might be tempted to switch to a “better” fund. Each switch incurs costs (like exit loads or taxes) and resets your compounding clock. Dhirendra Sir’s advice? “Keep your eyes on the horizon, stay diversified, and trust in your strategy.” This approach saves you from emotional burnout and keeps your portfolio on track.

The Power of Patience and Discipline

Mutual funds shine when you embrace their long-term nature. As Dhirendra Sir puts it, “Panic sells, but Indian investors aren’t buying it.” They’re not about instant riches but about building wealth steadily. Think of it like planting a mango tree—you don’t dig it up every season to check its roots; you nurture it and wait for the fruit. A disciplined approach, like investing ₹10,000 monthly in a diversified equity fund with a 10% average return, could grow to about ₹1,99,16,135 in 30 years, enough for retirement or a child’s education.

Systematic Investment Plans (SIPs) are a great way to stay disciplined, as Dhirendra Kumar highlights in Mutual Fund Insight. By investing a fixed amount regularly—say, ₹5,000 monthly—you benefit from rupee-cost averaging, buying more units when prices are low and fewer when prices are high. This smooths out volatility. For example, if you start an SIP of ₹5,000 in a mid-cap fund averaging 12% returns, you could have ₹1,01,40,885 after 20 years, even if markets fluctuate along the way.

When markets feel “flat” or headlines scream about crashes, like the 2024 FII narrative, Dhirendra Sir’s advice is clear: ignore the noise. Stick to your plan, choose quality funds (like those rated highly by Value Research), and let time and diversification work their magic.

Learing for Indian Investors

Investing is about consistency, not chasing excitement. Your mutual fund portfolio isn’t your stock trading portfolio. Mutual funds are your long-term partner, not a slot machine. For young investors or anyone starting out, here’s my advice:

- Choose Quality Funds: Pick diversified equity or balanced funds with a strong track record, like those recommended by Value Research.

- Set Up an SIP: Start small—even ₹2,000 monthly can grow to ₹9,32,248 in 20 years at 10% returns.

- Ignore the Noise: Don’t let market dips or trending funds on X sway you. As Dhirendra Sir says, “Stay diversified, and trust in your strategy.”

- Think Long-Term: Aim for 10–20 years to let compounding work. A ₹1,00,000 lump sum at 12% could grow to ₹9,64,629 in 20 years.

Let’s Hear From You

Have you ever been tempted to treat your mutual funds like stocks, switching based on a market dip or a trending fund? What was the outcome? Share your experiences with me at SocialInformer.data.blog—I’d love to keep this conversation going!

Leave a comment